In 2022, FHFA issued two new very significant policy announcements: a) a requirement that lenders deliver both the VantageScore 4.0 and FICO 10T credit scores; and b) the granting of discretion to lenders to drop to a bi-merge credit report from a tri-merge credit report.

Lenders will need to have a robust approach to manage these changes given the complexity and breadth of their impact. Identifying implementation steps and coordinating with partners beyond the GSEs will be key. For the first time in decades, these changes to the mortgage lending ecosystem will add new risk management, compliance, and governance responsibilities. Consumer education will be a necessity.

Although the implementation timeline has been delayed, we recommend lenders begin to prepare for the forthcoming changes by:

- Getting your input heard through involvement in the FHFA public engagement process

- Beginning to understand the operational impacts summarized below that will apply under almost any FHFA implementation approach

5 Areas of Lender Impact

- Credit Risk Scoring Model Validation

- Determine what model risk management regulations need to be adhered to

- Determine if historical back testing is necessary

- Test for regulatory (e.g., Fair Lending) and internal risk management compliance

- Coordinate credentialing and integration across the Credit Reporting Agencies (CRA)

- Policies & Processes

- Update proprietary underwriting policies

- Develop new reason code messaging and business rules

- Update processes to handle multiple GSE pricing grids

- Core Systems

- Update data fields, databases, and representative score calculations

- Update 3rd party data integrations

- Update user interfaces and workflows

- Consumer Communications & Reporting

- Create consumer education and communications around new credit score changes

- Update financial disclosures

- Budget & Implementation Plan

- Understand the level of effort from a cost, resource, and time perspective

- Allocate budget and resources for next year and beyond

- Develop a roadmap for implementation, testing, and roll-out

How did we get here?

Competition in credit scoring and expanding access to credit has been a priority for policy makers over the last decade.

Credit Scores

- In 2017, Congress passed Senate Bill 2155 to increase competition in credit scoring

- FHFA made a final decision in October 2022 to mandate the use of both VantageScore 4.0 and FICO 10T

Bi-merged Credit Report

- In 10/24/2022 FHFA issued a regulatory action ruling to allow for use of a bi-merged credit report

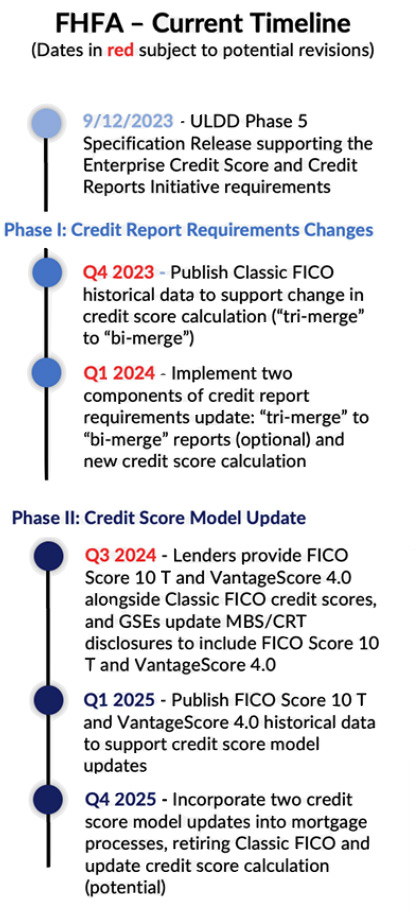

Where are we now?

On 9/11/2023 FHFA announced:

- A delay in the implementation timeline for the bi-merged credit report

- A public engagement period to gather additional industry input to ensure successful implementation