BACKGROUND:

On January 14, 2021, the Treasury Department and the Federal Housing Finance Agency (FHFA) amended the GSE’s Senior Preferred Stock Purchase Agreements (SPSPAs), which shape the terms in which Treasury supports Fannie Mae and Freddie Mac. This analysis looks at how the caps on the GSE’s “Acquisition of Certain Loans” can disproportionately impact homebuyers.

Among other constraints, the amendment to the GSE’s SPSPAs puts a cap (6% Purchase, 3% Refinance) on above 45% DTI (debt-to-income), above 90% OLTV (original loan-to-value) and below 680 FICO score loans. The amendment states:

“The GSEs will limit the acquisition of single-family mortgage loans with multiple higher risk characteristics at their current levels. A maximum of 6% of purchase money mortgages and maximum of 3% of refinancing mortgages over the trailing 52-week period can have two or more higher risk characteristics at origination: combined loan-to-value (LTV) greater than 90%; debt-to-income ratio greater than 45%; and FICO (or equivalent credit score) less than 680.”

IMPACT ANALYSIS:

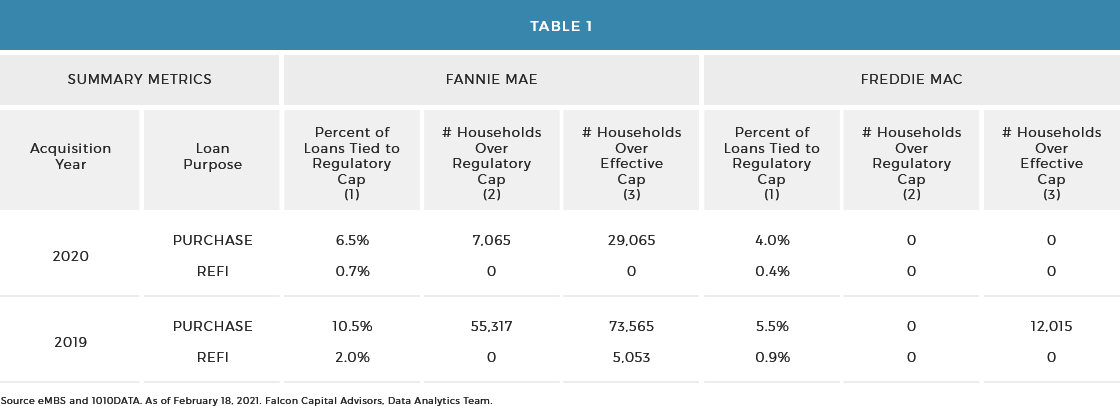

Falcon Capital Advisors’ Data Analytics Team calculated whether Freddie Mac or Fannie Mae would have been above or below these caps in the prior two years of each GSE’s acquisitions (2019 – 2020). We looked at a calendar year’s business to proxy FHFA’s trailing 52-week period. In Table 1, under the columns labeled Percent of Loans Tied to Regulatory Cap (1), we show each GSE’s percentages relative to the regulatory caps. Fannie Mae would have exceeded the cap over the prior two years. Freddie Mac would not have exceeded the caps, however, they skirted close to the cap in 2019.

We further estimated how many households would have been denied financing by each GSE in order to stay below the regulatory caps. In Table 1, under the columns labeled # of Households Over Regulatory Cap (2), we show our estimate of the number of households that put each GSE above the regulatory cap. Since Fannie Mae solely exceeded the cap, our estimate is that over 60,000 households would been denied credit by Fannie Mae over this two-year span in order to comply with the regulatory cap.

POTENTIAL GSE RESPONSES:

How will the GSE’s respond to the SPSPA amendment? We presume that it will be difficult operationally for the GSE’s and for their seller\servicer partners to shut off production at the moment a cap is breached. Consequently, the GSE’s are likely to manage compliance by setting target cap levels below the prescribed caps, putting the caps below 6% (for purchase money loans) and 3% (for refinance loans). We provide an estimate of the impacted households, assuming the GSE’s set their target caps 1.5 percentage points below the regulatory caps. This would make the “Effective Caps” 4.5% for purchase money and 1.5% for refinances. This is likely to be a low-end estimate but gives us a range of impacted households.

Referring once again to Table 1, in the column labeled # Households Over Effective Cap (3), we show the estimated number of impacted households, assuming the GSE’s manage to a cap below the regulatory threshold. The number of impacted households using the “Effective Caps” increases to over 100,000 households that would have been denied credit by Fannie Mae and Freddie Mae, combined, over the past two-year period. Implementing the “Effective Cap” juxtaposed with the regulatory cap provides us with a range of 60,000 to 100,000 impacted households over the prior two-year period.

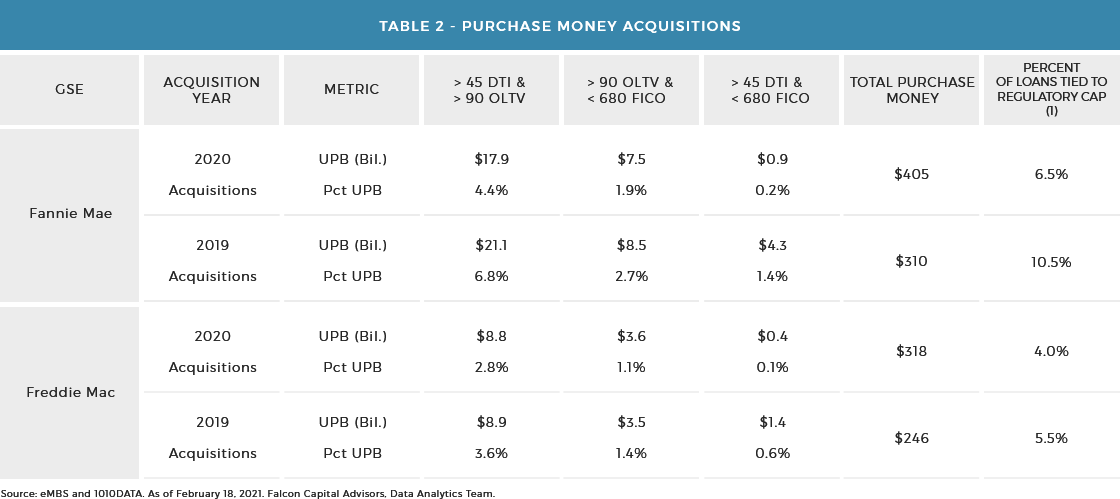

Table 2 shows the Unpaid Principal Balance (UPB) of the loans acquired in 2019 and 2020 for each of the three loan attribute combinations. We show this for Purchase loans only (excluded Refinances) because this category is the most impacted. In 2020, for instance, Fannie Mae acquired $17.9 billion in loans that were >45 DTI and >90 OLTV; $7.5 billion in loans that were >90 OLTV and <680 FICO, and $0.9 billion in loans that were >45 DTI and <680 FICO. This table is showing that the >45 DTI and >90 OLTV is the most impactful of the three loan attribute combinations.

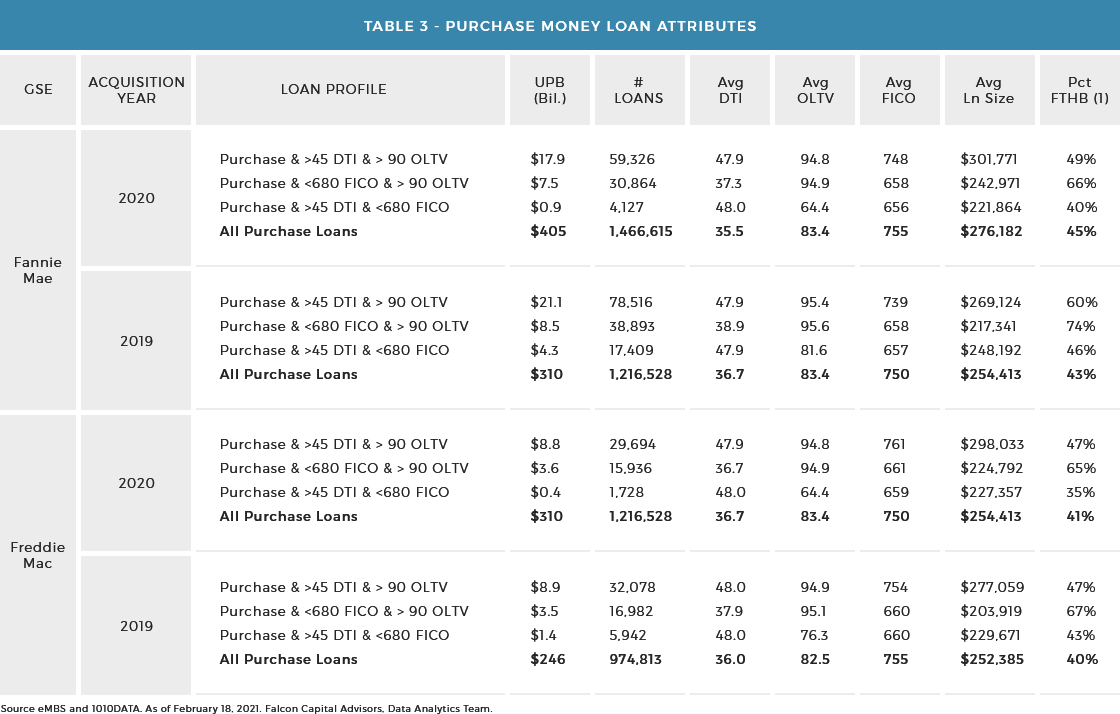

Table 3 shows the average DTI, OLTV, FICO, as well as average loan size and percent of loans that are First Time Homebuyers (FTHB) for each of the three loan attribute combinations and for all purchase loans. We show average loan size and percent FTHB to help us gauge whether these borrowers fit the GSE’s affordable housing goals. We believe the borrowers with high DTI, low average loan size, and are a FTHB are also likely to be counted towards the GSE’s affordable housing goals. Given the GSE’s strong commitment to the affordable housing goals, we also believe the GSEs are less likely to scale back on acquisition of loans that are goal rich.

Using All Purchase Loans as a benchmark to compare averages, we found the following profiles:

Loans with >45 DTI and >90 OLTV: These homeowners have roughly 10% higher loan sizes. Given the combination of above average loan sizes and high DTIs, we believe most of these homeowners have incomes above the threshold to meet the GSE’s Low-Income Home Purchase Goal for 2021. Given the large volume of >45 DTI and >90 OLTV acquisitions and the minimal affordability of this profile, it is very likely that these borrowers will be most impacted by the caps.

Loans with <680 FICO and >90 OLTV: These homeowners have roughly 15% lower average loan sizes and are very likely to be a first-time home buyer (FTHB). For example, Fannie Mae’s 2020 average loan size was roughly $243,000, 12% below Fannie Mae’s average for all purchase loans and 66% of the homeowners were a FTHB. This profile suggests that these homeowners align with the GSE’s affordable housing borrower profile (lower loan balances and mostly FTHB). Because the GSE’s are committed to supporting this segment of the market, it is less likely these homeowners will be impacted by the regulatory caps.

Loans with >45 DTI and <680 FICO: Given the low volume in 2020 of this profile (less than $1 billion in acquisitions for each GSE) relative to 2019 (Fannie Mae’s acquisitions were $4.3 billion), this indicates to us that both GSE’s (Fannie Mae in particular) have already scaled back on their acquisition of loans with >45 DTI and <680 FICO.

IMPACT TO HOMEBUYERS:

We estimated earlier that between 60,000 to 100,000 households would have been impacted had this regulation gone into effect in January 2019, and that borrowers whose loans are >45 DTI and >90 OLTV will be the most impacted. These homeowners have FHA as an alternative source of mortgage financing, but that option would come with a higher financing cost to the homeowner. In other words, if these homeowners can get an FHA loan, they will pay, on average, $3,750 more in upfront mortgage insurance fees under FHA, while saving, on average, $690 in annual interest payments. We are using Fannie Mae’s 2020 loan profile (average loan size of ~$300,000, OLTV ~95, and FICO ~740 ) to derive FHA and the GSE’s insurance fees. It will take roughly 5.5 years for these homeowners to breakeven ($3,750 divided by $690) by choosing the FHA option.

FEDERAL MORTGAGE PROGRAMS:

While we make no assertions on whether the caps are effective risk management tools for the GSE’s, we believe that these borrowers will simply shift their financing source from a conventional loan to getting an FHA loan, thereby keeping the risk on the government balance sheet. The net impact is higher financing costs to homeowners and the credit risk moving from the GSE’s to the FHA.

TABLE CALCULATIONS:

TABLES 1 AND 2

(1) Percent of Loans Tied to Regulatory Cap: Numerator = Acquisition UPB of any loan: [ >45 DTI and >90 OLTV ] plus [ >45 DTI and <680 FICO ] plus [ >90 OLTV and <680 FICO ] minus [ >45 DTI and > 90 OLTV and <680 FICO ]. Denominator = Total Acquisitions. By Purchase or Refinance Loan Purpose.

(2) # Households Over Regulatory Cap: Estimated from product of [ Percent of Loans Tied to Regulatory Cap minus Regulatory Cap, 6% for purchase and 3% for refinances, Max 0] times the number of loans acquired. By Purchase or Refinance Loan Purpose.

(3) # Households Over Effective Cap: Estimated from product of [ Percent of Loans Tied to Regulatory Cap minus Effective Cap, 4.5% for purchase and 1.5% for refinances, Max 0] times the number of loans acquired. By Purchase or Refinance Loan Purpose.

TABLE 3

(1) Pct FTHB: Percent First Time Home Buyer based on loan count.