From Hesitation to Transformation: How the Correspondent Lending Channel Can Help Drive the Future of eNote Adoption

A challenge to the widespread adoption of eNotes (i.e., promissory notes generated, presented, and signed electronically) has been getting broad participation from the correspondent lending channel. Originators who have correspondent aggregator partners that do not accept eNotes have been hesitant to implement eClosing solutions. The perception among such originators is that an insufficient number of their aggregators accept eNotes and therefore they won’t be able to get the best price possible for an eNote compared to a paper note. While originating lenders selling the majority of their loans directly to Fannie Mae or Freddie Mac, who each accept eNotes, have confidence there will be a buyer for their eNotes, lenders selling to multiple correspondent channel aggregators on a best execution basis often do not have this same confidence.

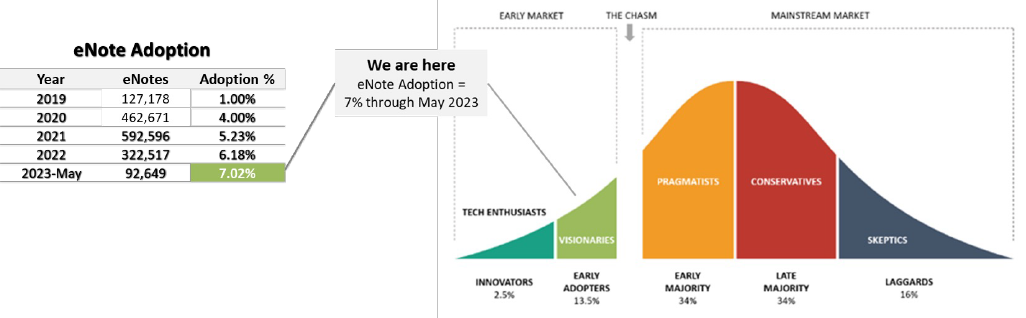

The aggregator adoption gap is one of the reasons overall eNote adoption has been slow, despite predictions that eNotes would have already become the norm. As depicted in the Technology Adoption Lifecycle figure below, moving eNote adoption from where we are today (<10%) in the Early Adopters phase3 to the majority of the market is a significant hurdle. Moving eNote adoption to the next phase may require a catalyst event or a series of market developments that motivate wider adoption. One of those developments will need to be significant progress in aggregator adoption.

1 Top 20 aggregators are estimated to account for most of correspondent channel volume based on GSE and GNMA Q1-2023 disclosure data that indicates ~90% of top 20 correspondent conforming loan volume is ultimately pooled into GSE and GNMA securities.

2 MERS® eRegistry data as of 6/1/2023.

3 Moore, G.A. (2014). Crossing the Chasm: Marketing and Selling Disruptive Products to Mainstream Customers. Harper Business.

A look at the top 20 aggregators who account for most of the correspondent channel loan volume1 reveals that only ~50% are listed on the MERS® eRegistry as transacting in eNotes2. We estimate that the market will need to hit 70 – 80% eNote adoption among the top 20 aggregators before the originator community will have the confidence in the secondary market necessary to rapidly move adoption forward.

So, what is holding up aggregators from adopting eNotes? Like the adoption of any technology there are numerous forces at work. In our industry we typically see less technology investment in a down market. This continues to be a factor even though this is a short-sighted rationale for remaining on the sidelines. A “chicken and egg” dynamic is also at work where aggregators are waiting for greater demand from their originators, and originators are waiting for broader aggregator adoption.

Perhaps we can break out of this cycle if the mortgage market has a better understanding of the benefits of eNotes. Help might also come from continued maturation of the overall eClosing ecosystem, such as through enhanced technology solutions, more system-to-system integrations, advancements in interoperability, the development of industry standards, or additional legal foundations like the SECURE Notarization Act.

For right now though, we expect that more aggregators will move to adopt eNotes as more market research and data on the benefits of eNotes becomes available. Recent origination studies have highlighted several areas of savings and advantages that can be applied to aggregators. Some of these benefits are:

Quality Control Review Efficiencies – eNotes bring significant efficiency gains to quality control review processes as data and document accuracy and completeness are enforced during the closing process. By leveraging digital verification and automation, aggregators can streamline workflows, reduce manual efforts, and expedite the loan review cycle. This results in time savings, improved accuracy, and more efficient resource allocation.

Faster Execution – eNotes enable faster execution, speeding up delivery time from the primary to secondary market by providing seamless transfer of ownership, eliminating physical document handling, reducing errors and omissions that delay processing, and enabling digital workflows.

Paper & Shipping Cost Savings – By adopting eNotes, aggregators can achieve substantial cost savings in paper and shipping expenses. The reduced need for physical storage space, courier services, and paper-related supplies leads to more efficient resource allocation and a significant reduction in associated costs.

Streamlined Communication & Issue Resolution – eNotes and digital closing packages streamline communication and issue resolution between aggregators and loan originators. They minimize back-and-forth exchanges, especially concerning closed loan packages, resulting in more efficient and effective collaboration.

Competitive Advantage – Investing in eNote technology positions aggregators for growth and competitiveness in the digital mortgage market, a market that will eventually overtake paper notes. Aggregators not participating in this rapidly growing market, which already constitutes 7% of GSE-eligible loans, risk missing out on a significant portion of the market as well as offering their customers more efficient service.

Custodial Certification Savings & Collateral Transfer – eNotes offer the advantage of auto-certification for loans that are pooled and sold to the GSEs. This eliminates a dependency on custodians for note certification, streamlining the process and reducing potential bottlenecks. Aggregators can expedite the certification phase, ensuring a smoother flow of loans to the GSEs without the additional requirement of custodial certification.

There are five key steps that aggregators can take to establish a successful eNote program and unlock the benefits of a digital mortgage process:

- Select and implement an eVault technology

- Define program guidelines and product eligibility

- Develop processes and procedures

- Update downstream data management to accommodate eNotes

- Complete and execute on a communications plan to customers

By establishing a successful eNote program, Aggregators can reap the benefits of a more streamlined and digital mortgage process, contribute to the growth and advancement of the industry, and foster a more efficient and modern mortgage ecosystem.

To receive expert assistance in establishing your eNotes program, reach out to Jim Voth at Falcon Capital Advisors’ Digital Mortgage Practice at [email protected].